The thought of owning your first home is undoubtedly exciting, but for a lot of people it can also feel daunting (and financially impossible), especially in London’s market. Thankfully, there are lifelines. Initiatives and schemes like Pocket and First Homes are designed to help you on your journey to homeownership by giving you a discount on your first home. The two are somewhat similar and sometimes confused but there are crucial differences, so in this blog we’ll be shedding some light on exactly what Pocket and the First Homes scheme are, and how they compare. It’s important for you to make an informed decision that aligns with your homeownership goals when choosing how to buy, so whether you’re exploring your options or ready to take the leap, this blog is a must-read.

What is the First Homes scheme?

The First Homes scheme is a government scheme that offers newly built homes at a minimum discount of 30% of the market price to first-time buyers and key workers in England. To be eligible, you must be a first-time buyer, purchasing the property to live in as your sole residence, and have a combined household income of £80,000 or less (£90,000 in London).

What is Pocket?

Similarly, Pocket provides discounted homes for first-time buyers – exclusively in London. Our properties are specifically designed for Londoners (those who make our vibrant city what it is – we call them city makers) who are struggling to get onto the property ladder. To be eligible, applicants must also meet certain criteria, including being a first-time buyer, having a maximum household income of £90,000, and, sometimes (when a scheme is first launched for sale), living or working in the borough of the development. Pocket offers well-designed, energy-efficient homes sold at 20% less than the market rate.

What’s the difference between Pocket and First Homes?

At first glance, these schemes can look very similar, but there is one key difference: the absence of the First Homes scheme in London. Now, before we jump to conclusions, it’s not that developers aren’t keen to build First Homes in the city, but it’s very difficult for developers to offer homes at First Homes discount levels in London. Pocket, however has a different model which does allow us to offer 20% discounted homes, still at 100% ownership. Rather than simply discounting standard new-build homes (as with First Homes), the Pocket model works because we have developed a unique and efficient one-bedroom layout designed to suit the needs and lifestyles of those looking to get onto the property ladder in London, which we are able to offer at a discounted price.

Ultimately, the decision between buying using the First Homes Scheme or buying with Pocket depends on individual circumstances, including financial considerations, lifestyle preferences (including whether you want to live in London), and housing needs. By weighing the pros and cons of each option, first-time buyers can make an informed choice that aligns with their homeownership goals.

Visit pocketliving.com and get started on your homeownership journey today. By creating your My Pocket account, you can explore the range of 20% discount, 100% ownership homes tailored for you.

Spring has sprung, Londoners! It’s that time of the year to bid adieu to winter and embrace the blue skies that have appeared. In this blog, we’ve curated a selection of the best spring events in London that you won’t want to miss. There’s a little something for everyone, so gear up to mark those calendars!

Foodies Festival (25-27 May)

The Foodies Festival began in Edinburgh in 2006 and has since hosted 14 festivals nationwide. Each event celebrates local food and drink, featuring artisan producers, street food traders, and regional food and drink producers. You can expect 200+ food stalls, tastings, workshops, live music, and a DJ setting the vibe. As far as spring events in London go, this one has to be the tastiest!

Sunday Jazz and Soul Lunch at Boisdale (every Sunday)

Indulge in a Sunday Roast experience at Boisdale, where a scrumptious 3-course lunch is accompanied by a live jazz show. Gather your friends and family and enjoy the perfect combo of good food and live entertainment.

Gold Bunny Hunt at Hampton Court Palace (23 Mar-14 Apr)

Another must-attend spring event in London this year is the Lindt Gold Bunny Hunt at Hampton Court Palace this Easter. You’ll have to find bunny statues among the flowers and match names to red ribbons to win a chocolate treat. The perfect Easter adventure for your family.

London Home Show (13 Apr)

The London Home Show, where the housing market meets urban living. This spring event in London gathers property experts, developers, and housing organisations, offering insights into affordable homes and first time buyer opportunities. This year, Pocket Living are attending, speaking to first time buyers about how they can land a 20% discounted home, don’t miss out!

London Coffee Festival (11-14 Apr)

The ultimate coffee celebration at The London Coffee Festival is back. It showcases London’s leading specialty coffee culture and hospitality scene. Boasting 250+ artisan coffee and gourmet food brands, interactive workshops, barista demonstrations, and unique features like Latte Art Live, this is every coffee fanatics dream.

RHS Chelsea Flower Show (21-25 May)

One of the most famous spring events in London, RHS Chelsea Flower Show, is back! Globally acclaimed garden designers, plant specialists, and florists will gather in one of London’s charming neighbourhoods to showcase the latest and greatest in garden designs and floral displays.

London Marathon (21 Apr)

Join the iconic London Marathon, a celebrated event since 1981, weaving through the city’s landmarks like Buckingham Palace and Tower Bridge. Whether you’re running or cheering from the sidelines, the atmosphere is unbeatable.

We hope this roundup has sparked your excitement and filled your calendar with spring events in London. From sipping coffee at the London Coffee Festival to experiencing the vibrant colours at the RHS Chelsea Flower Show, to finding yourself a 20% discounted home, this season is going to be a good one.

So, it’s officially 2024 and you’ve decided that this is the year you’re going to begin your homeownership journey. It may be tempting to hop straight on to Zoopla and start browsing homes, but unfortunately you’ve got a little way to go before that step, first you’ll need to save for your mortgage deposit.

In this blog, we’re uncovering the most practical and effective ways to save money in 2024 – NOT including sacrificing your social life or keeping your wallet under lock and key.

Set Financial Goals

Your first port of call is to set your financial goals. You’ll need to fully understand your budget in order know what exactly you’re aiming towards and how you’ll save for your mortgage deposit.

Understand your budget: Begin by evaluating your monthly income and spending. Differentiate between essential spending, like bills and food shops, and non-essential spending. This will help you allocate funds wisely whilst creating your budget.

Create a savings timeline: A well planned timeline will keep you on track and motivated during your savings journey. Make sure you set achievable goals and stick to them!

Potential costs and expenses: It’s important to be aware of costs that might creep up on you. Make sure you have an emergency pot with enough money to tie you over should you have any surprise expenses, like car trouble (or a last minute birthday present for your Mum).

Budgeting Tips

It’s one thing to understand your budget, now it’s time to implement those saving strategies.

Cut down on unnecessary expenses: Identify non-essentials, like unused subscriptions or impulse buys, and wave goodbye. Redirect those funds into your first home fund. It’s about creating space for what really matters.

Utilise budgeting apps for tracking: Budgeting apps such as Snoop and Emma will help you to stay on tracks and enable you too see all of your spending and upcoming payments in one place. Some will highlight wasteful subscriptions, and some give you ways to save based on where you spend.

Spending Habits

It’ll be tricky to save for your mortgage deposit if you’re still splashing your cash willy-nilly. Here are a couple ways you can rein it in.

Make informed purchasing decisions: It’s time to adjust your mindset to make every penny count. Instead of impulse buys, try digging into reviews, comparing prices, and snagging deals.

Explore affordable alternatives: Craving your morning latte fix from Gail’s or a fancy dinner out? Explore affordable alternatives! Opt for homemade coffee or a cosy night in with friends. Small changes add up, leaving more cash for your first home fund.

Income Boosting Strategies

As well as saving, it’s worth thinking about ways that you can boost your income to reach your mortgage deposit.

Exploring additional income streams: Consider exploring side hustles. Whether it’s freelancing, tutoring, or turning a hobby into cash, these additional income streams can fast-track your journey to homeownership.

Remember, saving for your mortgage deposit isn’t about skipping the fun stuff – it’s about making savvy choices that align with your goals. From budgeting to exploring side gigs, every step counts toward your dream home. So, sip your homemade coffee and know that each penny saved gets you closer to that front door key. Here’s to getting one step closer to saying “home sweet home”!

Visit pocketliving.com and get started on your homeownership journey today. By creating your My Pocket account, you can explore the range of 20% discount, 100% ownership homes tailored for you.

Welcome to Forest Road, E17! Located in the heart of Walthamstow, it features 90 one-bedroom Pocket homes, including adaptable options for wheelchair users and private terraces. These affordable homes in London offer the perfect blend of urban living, accessibility, and community.

In this blog, we’re showing you what Forest Road is all about and what exactly makes these homes so affordable… Architectural innovation, eco-friendly design, community spirit, and Walthamstow’s art and culture are just a step away.

We believe that everyone deserves the opportunity to own a home in the city they love, which is why Pocket offer 100% owned homes, available to eligible first time buyers for at least 20% less than the market value. Through innovative design, cost-effective construction, and government-backed initiatives, we’re making homeownership in London a reality for first time buyers. Forest Road is one of many of our schemes creating affordable homes in London, keep reading to learn more!

Location

Located in Walthamstow, ‘Britain’s coolest neighbourhood’, Forest Road offers culture, food to die for, and endless entertainment. Here’s why this location is perfect for modern urban living:

Hoe Street: Hoe street is located between the east and west of Walthamstow, and is pretty much the best of both worlds. You’ll find 5 star restaurants hidden between a greasy spoon and a yoga studio. So, whatever you’re in the mood for, you’ll find it here.

Commuters Paradise: With transport links surrounding you, you can take your pick between bus, train and your own two feet! Walthamstow central is a mere 12 minute walk away, and you can hop on the tube to Kings Cross in just 14 minutes.

Walthamstow Village: The oldest part of Walthamstow, Waltham village, is a Conservation Area on Orford Road. Take a stroll through the part of the neighbour hood and discover popular spots like Eat17 and The Ancient House.

Green Space: City maker or not, everyone needs a bit of fresh air. With beautiful green spaces like Lloyd Park and Walthamstow Wetlands just around the corner, morning walks and picnics in the park have never been easier.

Home Features

We carefully designed these Pocket homes to match the lifestyles of modern city makers. Here’s what to expect in these affordable homes in London:

Open-Plan Living: The open-plan living space not only makes your home feel more spacious, but also makes hosting that bit more enjoyable. Now you can strike up conversation with your guests whilst cooking up a storm!

Fully-Equipped Kitchen: Your sleek and modern kitchen includes a slimline laminate worktop, granite composite sink, built-in Beko appliances, a ceramic hob with stainless steel splashback, and more. Whether you spend hours in the kitchen, or prefer a takeaway, we’ve got you covered.

Stylish Wet Room: The bathroom is not only aesthetic, but also practical. It features a modern wet room with a walk-in shower and large-format tiles. Ideal Standard ceramics and a Corian vanity top add that touch of luxury.

Bedroom Comfort: The bedroom offers plenty of space for a double bed, bedside cabinets, and a wardrobe.

Energy Efficiency: Featuring highly insulated interiors, energy-efficient lighting, solar panels, and air source heat pumps, these homes reduce energy costs and minimise environmental impact.

Amenities

From evenings on the rooftop with friends, to growing veg in the allotment beds, Forest Road was designed to create a community. Here are some amenities in these affordable homes in London, to keep your everyday life interesting:

Community Rooftop Terraces: These affordable homes in London feature two communal rooftop terraces with views of Lloyd Park and beyond. These spaces are perfect for relaxing, evening drinks, or exercising.

South-Facing Courtyard Garden: The ground-level courtyard garden is the perfect place to connect with your neighbours. This south-facing garden has a variety of comfortable seating options and even some communal allotment planters for those green thumbs!

Spacious foyer: The entrance at Forest Road is a large and airy space intended to encourage residents to linger and converse whilst collecting post or heading in for the night.

Secure Bicycle Storage: In an eco-conscious age, we’re actively encouraging cycling. So whether you commute daily or simply enjoy a summers bike ride, you’ll know that your bike is protected in our secure bike storage.

Sustainability

Highly Insulated Homes: These affordable homes in London are highly insulated, meaning they efficiently retain heat. Not only will this keep you comfortable in those grisly winter months, it’ll also reduce your monthly energy costs.

Solar Power: Solar panels contribute to the electricity supply for communal areas which is a step towards cleaner, renewable energy sources.

Natural Light: Floor-to-ceiling windows throughout the development allow natural daylight to brighten up your living space and minimise the need for artificial lighting.

Air Source Heat Pumps: This scheme utilises air source heat pumps to provide renewable heating and hot water. This technology reduces our carbon footprint whilst making certain you’ll be comfortable.

Brownfield Site Development: The homes are constructed on an urban brownfield site. By reusing existing sites, we’re helping to protect London’s Green Belt and reducing new construction on untouched land.

Floor Plans and Pricing

These affordable homes in London start from just £298,000! To view the full price list, click here.

Visit pocketliving.com and get started on your homeownership journey today. By creating your My Pocket account, you can explore the range of 20% discount, 100% ownership homes tailored for you.

New builds are great for a number of reasons. There’s less maintenance, less risk, and on the whole, less to worry about. But as with moving into any new home, sometimes they feel a tad… well, characterless. It’s important that when you enter a new space you make it your own, and you’ll be pleased to hear that adding a bit of warmth and personality to your home doesn’t require emptying your pockets! Read on to reveal how to add character to a new build on a budget.

Colour isn’t just for the eccentric, it can instantly turn your new build into a home. Here’s how you can embrace colour and add some personality into your new home…without sending your budget into a spin.

Colourful Walls: There’s no quicker, more budget-friendly way to add character to your new build than by paint. Choose a bold coloured paint or wallpaper to create a focal point in your living room or bedroom. Whether it’s a deep green or a bright yellow, a pop of colour can make all the difference.

Furniture: If bright walls aren’t your thing, consider adding colour through furniture. Statement sofas, eye-catching chairs, or colourful coffee tables can liven up your living space just like that.

Accessories: Sometimes, it’s the little things that make the biggest difference. Cushions, throws, rugs, and art in bold, contrasting colours can be added to your décor. Don’t be scared to mix up colours and patterns to find your style.

2. Statement Lighting

An empty, uninspiring room can quickly turn into a space filled with personality by simply changing the lighting.

Lamps: When it comes to adding character, Floor and table lamps are your best friends. Look out for unique bases or colourful lampshades to add some pizzazz.

Second hand finds: Charity shops and online marketplaces often hide unique and affordable treasures. Keep an eye out for vintage finds like chandeliers and remember, with a fresh coat of paint or some DIY, you can turn these almost anything into a statement piece.

Bulbs: Sometimes, it’s the bulbs themselves that can be the star of the show. Edison bulbs, for example, offer a vintage, industrial look. Or opt for colourful, energy-efficient LED bulbs to add a touch of whimsy.

3. Vintage and Second Hand Finds

Here’s how to add that vintage charm into your home without emptying your pockets:

Charity shops: Dive into local charity shops and markets for hidden gems. The of the hunt itself is part of the fun, and you’ll be amazed at the items you can discover on a budget to add character to your new build.

Online Marketplaces: With the rise of online marketplaces, vintage finds are easier than ever. Sites like Etsy, eBay, and Facebook Marketplace offer a vast array of affordable vintage furniture, décor, and accessories. Pro tip: Set up alerts for specific items or styles you’re seeking.

Upcycling Projects: Embrace your inner DIY enthusiast by upcycling vintage furniture or décor. A fresh coat of paint, new hardware, or minor repairs can breathe new life into old pieces. Plus, you’ll create something entirely unique in the process.

4. Houseplants

Adding character is about more than furniture and paint – it’s also about creating an atmosphere and house plants are an easy way to do just that. Not only do they purify the air and bring nature indoors, but they also add a touch of personality and cosiness to your space. And you don’t need a green thumb or a big budget to enjoy the benefits.

Start with low-maintenance options like snake plants or pothos vines. They’re fine in almost any light condition and can handle a little neglect.

For a pop of colour, consider flowering plants. You can find budget-friendly options like marigolds, petunias, or African violets.

Repurpose old containers or second hand pots for a shabby-chic look. Mix and match containers of different shapes and sizes for a more dynamic display.

5. Textiles

If you really want to know how to add character to a new build, look at the smaller details. Textiles, for example, have the ability to turn a plain room into a cosy haven or a vibrant gathering place. Here’s how you can work your magic with fabrics:

Curtains: Opt for curtains with bold patterns, rich textures, or subtle sheens to set the tone for your space. Whether you’re into boho or minimalism, there’ll be a fabric for you……

Rugs: A well-chosen rug can be a room’s centrepiece. Look for rugs that not only add colour but also texture. Layering rugs can create depth and intrigue, too. Plus, they feel great underfoot!

Bedding: Don’t forget about the bedroom! Crisp white sheets and neutral bedding create a tranquil atmosphere, while vibrant duvet covers and patterned pillows add a bold and energising touch. Who knew your bed could be such a blank canvas!

Embrace colour, dabble with lighting, explore vintage finds, bring in the greenery, and cosy up your space with textiles. These are your tools, and adding character has never been more budget-friendly. Whether it’s through an accent wall, a thrifted lamp, or a touch of nature, it’s all about turning your new build into a space that you’ll love.

In a world filled with clickbait headlines and seemingly endless debates about the right time to buy a home, it’s easy to feel like you’re caught in a whirlwind of uncertainty. But guess what? Amid all the noise, there’s one simple truth that stands tall and steadfast: Now could very well be the perfect time for first-time buyers to embark on their homeownership journey. We interviewed seasoned Mortgage Advisor, Anthony Hall, to explore why, despite what you might have heard about mortgage interest rates, the time to buy is now.

Current Market Overview

Let’s start with the big question: Is now the right time to buy? To find out, we’re diving deep into the mortgage market with the guidance of Anthony Hall, an expert with 16 years of experience in the mortgage industry, including 12 years helping Pocket buyers onto the ladder.

What are Mortgage Rates Today? The last update on the base rate was in September 2023, when the Bank of England maintained it at 5.25%. The base rate remaining unchanged at 5.25% is good news for the mortgage market as new borrowers are boosted by the base rate being held as lenders use the BOE base rate when calculating their stress test rate. When the rate rises this in turn reduces the amount of borrowing available to purchasers. Mortgage borrowers on variable rates or trackers will be breathing a sigh of relief as they will not see an increase in their monthly payments which has gone up 5 times this year!

According to Anthony, “the current mortgage market is, I would say, currently stable.” However, it’s been a journey to this point. Following a rollercoaster ride of interest rate fluctuations, the market has landed on a steadier path. What once felt like financial whiplash due to volatile rates has now evolved into a more predictable landscape. Factors like inflation, the Bank of England’s rate adjustments, and lender responses have all played their part in the market’s ups and downs.

Historical Mortgage Rate Trends Let’s take a trip down memory lane, shall we? Anthony’s expertise is instrumental in navigating these waters and he highlighted an essential point: the current rates, while seemingly high in today’s context, are comfortably within the historical average. For the past quarter-century, the norm has hovered around 5%. The record-low rates we’ve grown accustomed to in recent years following the 2008 financial crisis were the real anomaly. Yes, we’ve been spoiled by those low rates, but in reality we’re returning to a more typical interest rate scenario, akin to that of 2008 when rates exceeded 7% for some buyers. We’re heading toward a market where 3% to 5% interest rates are the new normal. The good news? We’re not expecting rates to crash anytime soon. It’s all about settling into a healthier, more sustainable range.

What does this mean for the average homebuyer? In Anthony’s words, “if you can afford a mortgage now and get a fixed rate for five years, your rate won’t change during that time.” It’s about securing financial predictability. While the crystal ball remains elusive, the outlook is one of gradual, measured rate increases. The takeaway? Buying a home today, with a manageable fixed-rate mortgage, can set you on a path to financial stability and potential long-term gains. History has shown that property in the UK consistently appreciates, and despite occasional dips in reported growth rates, the underlying value remains robust.

The Downsides of Waiting to Buy a House

Here’s the deal: when you put off buying a home, you’re not just hitting the pause button on homeownership. You’re also missing out on a world of potential benefits. Let’s delve into why waiting might not be the best move.

First and foremost, it’s all about opportunity. So you’ve got your eye on a brand-new property, and it ticks all your dream home boxes. The catch? New builds tend to have limited availability. So while you’re contemplating your options, someone else might swoop in and claim your ideal property. When it comes to securing that perfect place, hesitation could cost you more than you think.

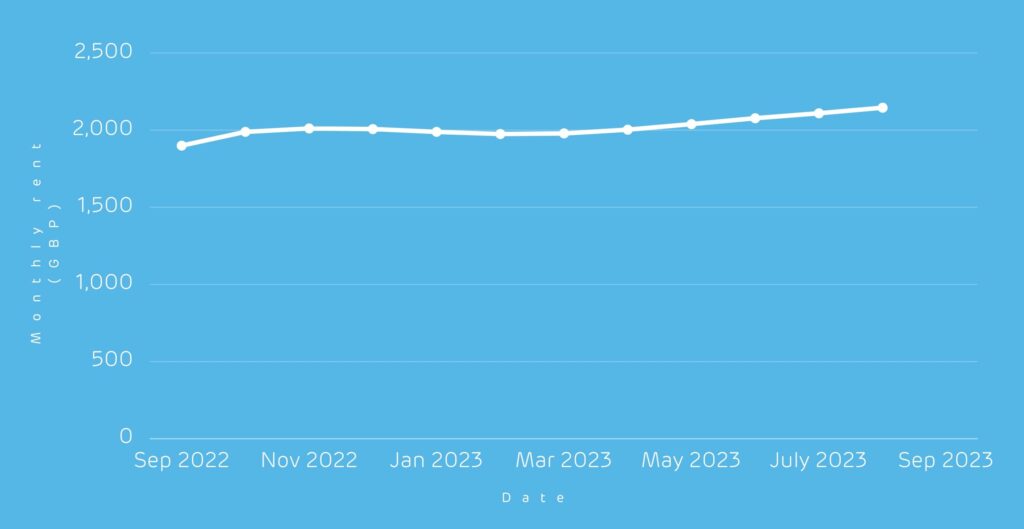

Now, let’s talk finances. Renting is like pouring your hard-earned money into a bottomless pit. Every month, you’re handing over your cash without building equity or investing in your future. Plus, there’s the looming spectre of rent increases. As interest rates go up, landlords may decide to pass those costs onto you. So that sweet rental deal you’ve got today might not look so great in the near future.

Average rental value for new tenancies in London according to Home Let Rents in London have increased by 13.0% compared to last year.

Security matters, too. Renting means you’re at the mercy of your landlord’s plans. They might decide to sell the property, forcing you to pack your bags and find a new place to call home. That’s hardly the stable and secure future you envision, is it?

Then there’s the question of interest rates. Anthony puts it bluntly: “We don’t know what’s going to happen definitively with interest rates.” Waiting for them to drop might leave you in a never-ending waiting game. While rates aren’t likely to return to the super-low levels of the past, they’re also not skyrocketing uncontrollably. So the real question is: when do you decide it’s the right interest rate for you? The sooner you start paying down your mortgage, the quicker you’re building equity and securing your financial future.

So, when you consider all these factors, it’s pretty clear – waiting might not be the wisest move. You could be missing out on the perfect property, wasting money on rent, and forfeiting the security and equity that come with homeownership. It’s time to seize the day and embark on your homeownership journey. Your future self will thank you.

Is now the right time to buy for you?

There are a number of things to consider when contemplating if now really is the right time for you to buy.

Anthony stresses the importance of understanding your current financial standing. He remarks, “A lot of people don’t realise that they are in a position to buy because they haven’t been assessed or received proper advice.” The first step he suggests is getting a clear picture of your affordability. Start by creating a budget planner. Analyse your recent pay stubs and bank statements, meticulously documenting your income and expenses. This budget planner becomes your invaluable tool for determining what’s genuinely affordable each month. Anthony recommends, “Look for a mortgage affordability calculator online to assist you in this process.”

Credit Check

In addition to your budget, your credit report plays a pivotal role in the affordability equation. Anthony advises, “Take a close look at your credit history and reports to understand where you stand.” Outstanding commitments, such as car loans and credit card balances, impact your borrowing capacity, which, in turn, defines what you can afford to purchase. Keeping your credit history in check ensures you’re in the best position to secure a mortgage that aligns with your goals.

Life Goals and Needs

Here’s the exciting twist – your decision to buy a home isn’t just about market trends. It’s about your unique life goals and needs. Anthony’s take? “The right time to buy is when you can afford it.” Waiting for the stars to align in the market can be like waiting for a unicorn sighting – uncertain and lengthy. Meanwhile, you could be pouring your hard-earned cash into rent or living in a place that doesn’t quite fit your vibe. So, if your life goals and needs harmonise with homeownership, don’t wait for the market’s permission slip.

Addiscombe Grove CR0, Croydon

The Decision to Wait

Once you’ve conducted your affordability assessment and it aligns with your current budget, the question arises: should you wait for market conditions to shift, or is it time to take the plunge? Anthony offers a clear perspective: “The right time to buy is when you can afford it.” Waiting for interest rates to fluctuate or for headlines to declare an optimal moment can be a protracted, uncertain endeavour. During this wait, you could be spending substantial sums on rent or residing in a place that doesn’t quite suit your preferences. Anthony reinforces the point that “if you can afford to buy, waiting for market changes might not be the best course of action.”

3 Tips for first time buyers

In essence, the decision to buy a home is not solely driven by market dynamics but by your unique circumstances and financial capacity. Anthony suggests, “Speak to experts who understand the intricacies of interest rates and mortgages. They can provide tailored advice and guide you toward a decision that’s right for you.”

Tip 1: Income Insights First off, your income – it’s a game-changer when it comes to mortgages. Anthony says, “Different lenders treat your income differently.” If you’re the proud owner of a P60, get it ready. If you’re self-employed, gather those tax overviews and financial statements. And hey, if you’ve got an accountant, give them a shout – they’re like financial wizards for these kinds of things. Understanding how your income plays into the mortgage puzzle is your ticket to making the right moves.

Tip 2: Savings Savvy Now, let’s talk savings – the magic potion for a hefty deposit. Anthony advises, “Understand how much savings and deposit you’ll potentially have access to.” Whether it’s a generous gift from family or friends, get all the deets lined up. The more you know about your deposit, the clearer the borrowing picture becomes. Plus, it’s like having the answers before the big test – confidence booster, right? Oh, and here’s a pro tip: Check your credit report. Grab one for free from credit agencies, scrutinise it, and if you spot any hiccups, sort them out. Clean credit makes for smooth sailing in the mortgage world.

Tip 3: Budget Brilliance Lastly, let’s get down to brass tacks – your budget. Anthony’s top advice? “Put together a detailed budget planner.” Knowing how much you can comfortably spend each month is like having a superpower. It not only helps you choose the right mortgage but also lets you explore the mortgage products that are tailor-made for you. So, dive into your expenses and income, and emerge with a budget that’s your trusty sidekick on this homeownership journey.

In the world of real estate, the waiting game often leads to missed opportunities. The current mortgage market is stable, with rates favourable compared to historical trends. Hall emphasises that homeownership offers security, equity, and freedom from the rent cycle, So why wait for the perfect moment if you can make it now?

Visit pocketliving.com and get started on your homeownership journey today. By creating your My Pocket account, you can explore the range of 20% discount, 100% ownership homes tailored for you.

London’s first time buyers have made it clear that having access to outdoor spaces is really important. In our post-COVID-19 world, city makers have felt first-hand the difference this can make.

Our design ethos is to build homes designed for city living, and a key element of this is to include shared spaces in every Pocket Living development. Ample communal spaces encourage a sense of community, and our rooftop terraces have become particularly popular. Here are a few of our favourites.

Bridget (37) has always dreamed of putting down roots in London, but for the past three years she has struggled to find a home within her budget.

“I am originally from North London, and most of my friends and family still live here, so it was always a goal of mine to be able to afford my own home nearby. I rented on and off for 10 years and found searching for affordable and suitable apartments became quite hard work, which really forced me to start looking for my own home. But it wasn’t easy”, says Bridget.

It’s that time of year again where we all start thinking about sprucing up our homes for the warmer months ahead. If the thought of spring cleaning fills you with dread, then read on for 10 tips that will make the process a breeze!

So, you’re a first time buyer. You dream of getting onto the property ladder but it seems totally overwhelming… sound familiar? We can help! Buying your first home can be daunting, but it needn’t be. Here we have broken down the process so you have a step by step guide on how to buy a home.